Leeham News and Analysis

There's more to real news than a news release.

Paris Air Show Preview: Airbus

Subscription Required.

Introduction

May 3, 2015, c. Leeham Co. The Paris Air Show is June 15-19 for the trade/industrial portion. Beginning this week, Leeham News and Comment will provide our

![]() Market Assessment and insight about what to expect. We begin this weekly exercise by looking at Airbus. Future posts will look at Boeing, Bombardier, Embraer and other major players at the PAS.

Market Assessment and insight about what to expect. We begin this weekly exercise by looking at Airbus. Future posts will look at Boeing, Bombardier, Embraer and other major players at the PAS.

Summary

- First, an overarching look at what to expect;

- What to expect for Airbus at the show;

- The future of the A380neo;

- Outlook for the A330ceo/neo; and

- Outlook for the A321LR.

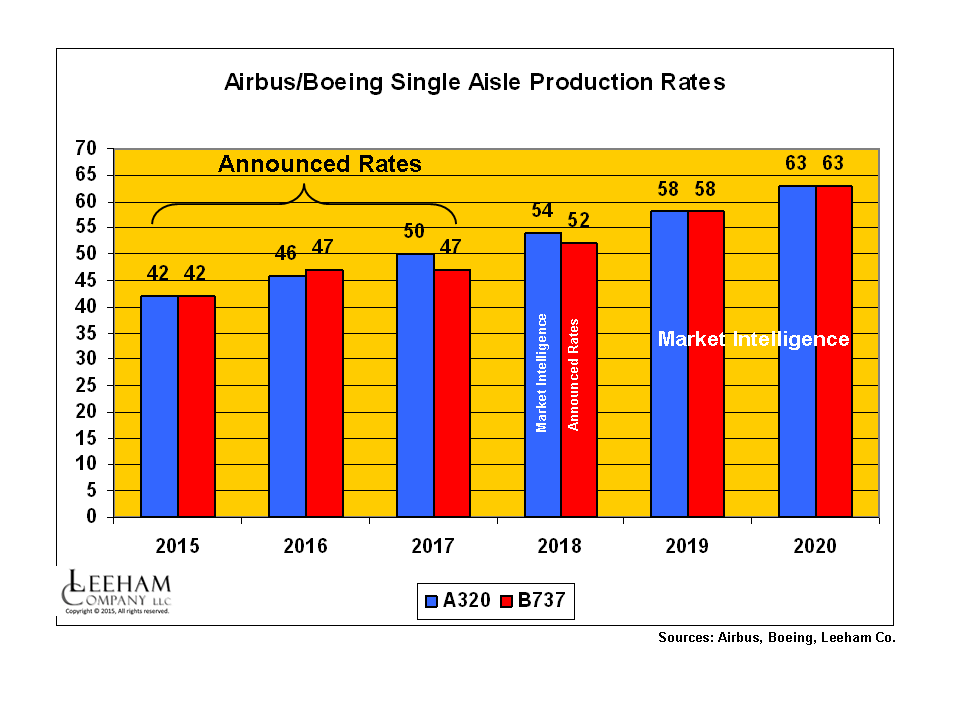

Production rates on single-aisles keep going up, up

Figure 1. Airbus and Boeing production rates for the A320 and 737 lines are going up as announced rates and rates under consideration go to lofty levels. Click on image to enlarge.

Subscription Required

Introduction

March 3, 2015: c. Leeham Co. Production rates for single aisle airplanes continue to go up for the Big Two, following the Airbus announcement last week that the A320 rates will go to 50/mo in 2017 and officials are considering going to more than 60/mo.

We’ve previously reported that Airbus already has notified the supply chain to be prepared to go to 54/mo in 2018.

Rate 50 will propel Airbus ahead of Boeing, which will briefly be ahead of Airbus when the 737 production rate goes to 47/mo next year, compared with the Airbus plan to take A320 rates to 46/mo next year. The two companies are at parity this year. (Figure 1.)

Summary

- Bombardier, COMAC and Irkut add to supply by 2020, but impact will be minimal.

- No 747-8 deliveries scheduled in 2018. We see program termination coming very soon.

- A330ceo production rate reduced, higher rate for 787 than announced.

- We see short-term Airbus advantage coming in wide-body production rates as A350 ramps up. We stick with our call that 777 Classic rates have to come down.

- We reduce A380 production rates in our estimates.

Airbus/Boeing production rates forecast through 2020

Subscription Required.

Introduction

Feb. 3, 2015: Boeing out-delivered Airbus in 2014, for the second year in a row, as the 787 program improved in delivery rates and before the A350 made its first delivery in December.

Topping Airbus in deliveries allowed Boeing to claim it is the world’s leading ![]() commercial airplane manufacturer. By the delivery metric, Boeing is. By orders, Airbus came in first again, maintaining a decade-long lead.

commercial airplane manufacturer. By the delivery metric, Boeing is. By orders, Airbus came in first again, maintaining a decade-long lead.

The A350 ramps up its production this year even as the A330ceo rate begins to come down at the end of the year and further next year. Boeing vows to maintain the current production rate of the 777 Classic at 100/yr. The 747-8 rate is declining. And both companies are ramping up rates of the single-aisle airplanes.

The production wars continue.

Summary

- Airbus is forecast to out-produce Boeing by 2018.

- Boeing’s ramp-up of the 737 line will drive the delivery stream.

- The 737 rate may hit 63/mo by 2020.

- Airbus will likely match.

Airbus/Boeing duopoly single-aisle is safe well into 2030 decade

Subscription Required

Introduction

Dec. 28, 2014: Two challenges to the duopoly of Airbus and Boeing in the 150-220 seat single-aisle sector move forward in development in 2015, but neither is in a position to be a threat for the balance of this decade, nor even in the next.

Both challenges, the COMAC C919 from China, and the Irkut MC-21 from Russia, will for various reasons fall short of the Airbus A320/321 and Boeing 737-8/9 and plans to design the next generation new single-aisle airplane.

Summary

- The C919’s chief advantage was eliminated when Airbus and Boeing moved to reengine the A320 and 737 families.

- C919 retains pricing advantage but won’t overcome duopoly dominance.

- By the time the C919 enters service, Airbus and Boeing will have the second generation of LEAP and GTF engines available.

- The MC-21 takes into account better passenger comfort through a wider fuselage, but engines will be no better than those used on Airbus and Boeing.

- The MC-21 sales potential will be highly limited because Russia still hasn’t become a full trading partner due to political direction.

MTU investors day: views of its engine programs, future airplane timelines; separately, Embraer COO interview

Figure 1. Technical milestones have been passed on PW GTF programs for the applications on Bombardier, Airbus, Mitsubishi and Irkut airplanes and are approaching for Embraer. Source: MTU Investors Day. Click to enlarge.

Nov. 30, 2014: MTU Investors Day: MTU is a major participant in engine development and supplies, participating on the GEnx, GTF and GEnx program. It’s also a member of the joint venture in International Aero Engines and it’s a major player in the aftermarket Maintenance, Repair and Overhaul (MRO) sector, providing a serious competitive alternative to the aftermarket contracts offered by the engine OEMs. Its held an investors day conference Nov. 25. Highlights included:

- Milestones have been passed on the Pratt & Whitney Geared Turbo Fanengine for the Bombardier CSeries, Airbus A320neo family, the Mitsubishi MRJ and Irkut MC-21; and are on schedule for the Embraer E-Jet E2.

- The success of the GTF is requiring huge production commitments.

- The large number of airplane/engine programs require a major ramp-up of production during the next few years.

- The major investment in new engines is largely over for now, leading to the expectation of long-term revenue from MRO.