Leeham News and Analysis

There's more to real news than a news release.

Leeham News and Analysis

Leeham News and Analysis

- Does an A220-500 need a new wing and engines? Part 4. July 3, 2025

- GE testing of giant GE9X engine aims for maturity at entry into service June 30, 2025

- Bjorn’s Corner: Air Transport’s route to 2050. Part 28. June 27, 2025

- Parent agency, FAA often at odds as politics outweighs safety June 26, 2025

- Electric Flight and the Ugly Duckling June 25, 2025

This is a pivotal year for the A380 as Airbus considers neo, PIPs

Introduction

March 15, 2015: This is a pivotal year for the future of the Airbus A380.

Tim Clark, the president of Emirates Airline, increased the pressure for development of an A380neo when he said he’d buy up to 200 of the prospective re-engined airplane, potentially doubling the number of neos he previously said he’d buy.

It was widely expected that if Airbus proceeds with a neo, Rolls-Royce will provide the engine. Market Intelligence, however, indicates development of the Advance engine may be running into challenges. Airbus is now talking with Engine Alliance about upgrades to the GP7200.

Summary

- Customers take wait-and-see approach to prospect of a New Engine Option.

- Mixing engine types a consideration for some.

- Some at Boeing quietly rooting for Airbus to proceed.

Redefining the 757 replacement: Requirement for the 225/5000 Sector, Part 5.

By Bjorn Fehrm

Subscription required

Introduction

11 March 2015, c. Leeham Co: After having analyzed the different alternatives which would be available to Boeing for its Middle Of the Market, MOM, studies and having singled out the most competitive configurations, we will now add revenue to the equation. In the work to establish Cash and Direct Operating Costs for the aircraft, we saw which variant had the best cost for a certain capacity and utilization. We could not see which aircraft would be the most profitable however; this requires that we bring in the revenue side.

Revenue management analysis of different aircraft types on an airlines network is a science in it selves. Sophisticated fare class strategies with connected marketing activities makes such studies elaborate and beyond the scope of our analysis. Our primary goal is to understand the difference in operational efficiency of a single versus dual aisle aircraft with the same seating capacity. For this, a simpler average margin concept will work that shows us the effects of single versus dual aisle for aircraft margins in the MOM segment.

Summary

- We select based on Cash and Direct Operating Costs the best aircraft for the different market segments.

- To understand the revenue earning capability of the different alternatives we introduce a revenue model which takes into account aircraft utilization.

- With the costs and the revenue side represented we can develop a good understanding for the cross over between single and dual aisle for MOM.

- We will use this knowledge as we subsequently look into Airbus response to what Boeing would bring to the market.

Redefining the 757 replacement: Requirement for the 225/5000 Sector, Part 4.

By Bjorn Fehrm

Subscription required

Introduction

08 March 2015, c. Leeham Co: In the third part of the article series around the need for a more capable solution for 180-240 seats and 5,000 nautical miles, we compared different clean sheet single and dual aisle aircraft to the Airbus A321LR and Boeing’s 787-8, the two aircraft that form the border to the segment.

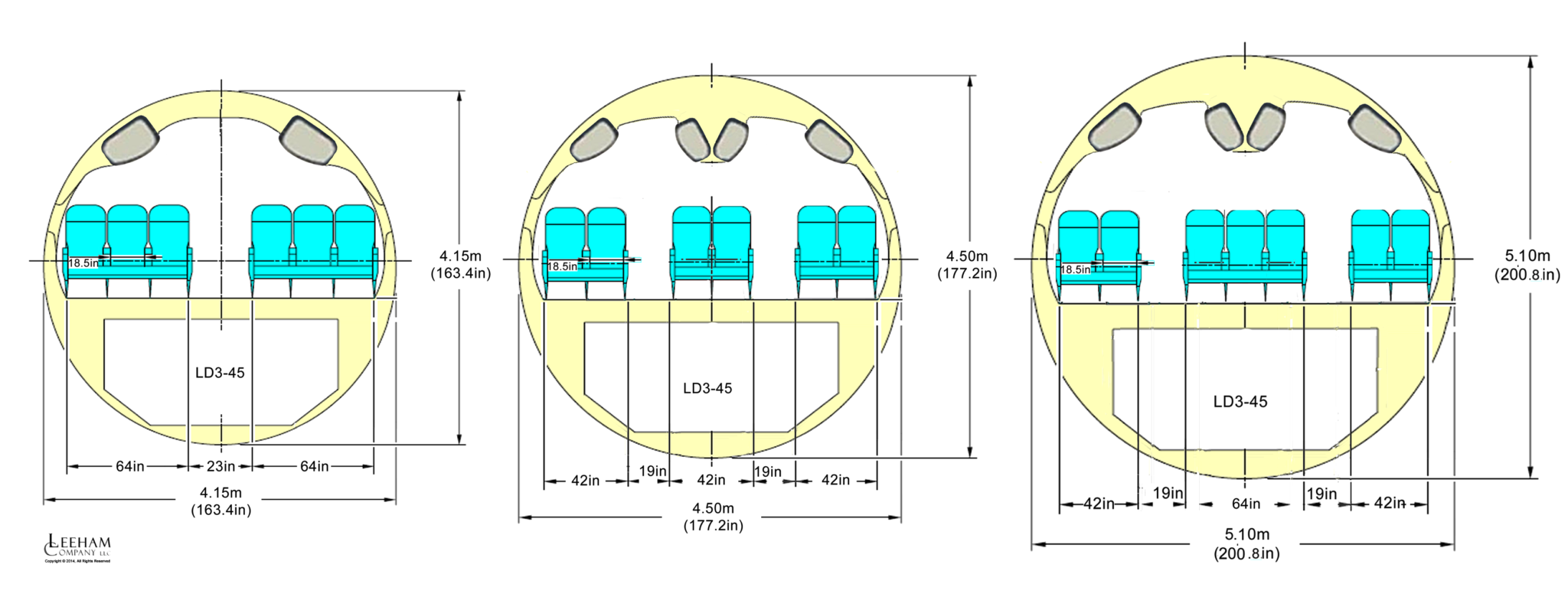

We could see that a single aisle aircraft started to have trouble with weight at around 220 passengers using our normalized seating rule set. This would with normal OEM seating rules be around 230-240 passengers. At the same time the dual aisle aircraft becomes stronger the more seats one assumes. The reason is their thicker fuselage, Figure 1, lends itself better to aircraft which passes 50 meters/160 feet in length.

Figure 1. Cross sections for our studied clean sheet designs; NSA6 (New Single Aisle 6 abreast), NLT6 (New Light Twin 6 ab.) and NLT7. Source: Leeham Co.

Their advantages in boarding and deplaning then starts to outweigh their disadvantages in weight and drag. This trend is explored further in this part where we add Cash Operating Cost, COC and Direct Operating Cost, DOC, to the analysis.

Summary

- The trends seen for NAS6, NLT6 and NLT7, our Middle Of the Market, MOM, models in the segment 180 to 240 passengers gets further reinforced when we go to COC and DOC.

- A factor supporting this is the broader spread of fixed and semi-fixed costs over larger aircraft seat numbers.

- Another is that the shorter ground turn-around time for dual aisles increases the utilization for the aircraft, once again forming a broader base for fixed and semi-fixed costs.

- Introducing CFRP for the fuselage brings clear gains in weight and therefore operating costs. Key for its inclusion in the MOM designs will be the manufacturing advances that will have been made by 2025.

Redefining the 757 replacement: Requirement for the 225/5000 Sector, Part 3.

By Bjorn Fehrm

Subscription required

Introduction

04 March 2015, c. Leeham Co: In the first and second part of the article series around the need for a more capable solution for 180-240 seats and 5000 nautical miles, which we have labeled the 225/5000 Sector, we went through the derivatives we have analyzed as competitors to Airbus A321LR and showed why none of them are effective as a Boeing solution.

We also looked at the wetted area and weight for our common single and dual aisle aircraft. These parameters are the principal components that determine an aircraft’s efficiency given a certain engine efficiency. We also developed the market picture, outlining a substantial market by the time of entry into service of a clean sheet design by 2025, given that certain market requirements could be fulfilled.

We will now project different solutions to the requirements, thereby utilizing the preliminary design part of our proprietary aircraft model. We will look at three different cabin configurations in four different size classes between 180 to 240 seats and calculate size and weights and the resulting efficiency of the different variants. Against the key data for these different aircraft and their operational efficiency we will be able to postulate what will be the next move from Boeing and Airbus in this segment.

Summary

The findings in this our third article include:

- Aircraft capacity and size for 12 different possible aircraft, named NAS6, NLT6 and NLT7 each in the variants 180, 200, 220 and 240 passengers.

- With this collection of characteristics it will be possible to compare the efficiency and costs for the different sizes and to see how competitive a wider dual aisle aircraft will be in this segment compared to a single aisle.

- In a subsequent article will be compare the operational characteristics of these aircraft thereby also covering the increased revenue potential with a dual aisle aircraft compared to a single aisle.

Production rates on single-aisles keep going up, up

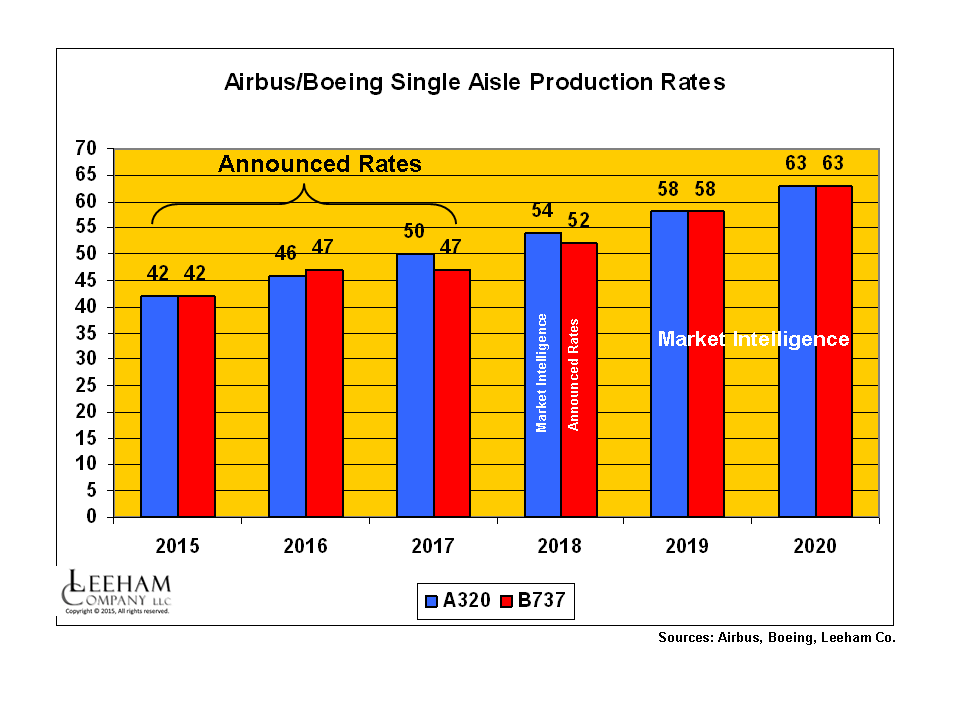

Figure 1. Airbus and Boeing production rates for the A320 and 737 lines are going up as announced rates and rates under consideration go to lofty levels. Click on image to enlarge.

Subscription Required

Introduction

March 3, 2015: c. Leeham Co. Production rates for single aisle airplanes continue to go up for the Big Two, following the Airbus announcement last week that the A320 rates will go to 50/mo in 2017 and officials are considering going to more than 60/mo.

We’ve previously reported that Airbus already has notified the supply chain to be prepared to go to 54/mo in 2018.

Rate 50 will propel Airbus ahead of Boeing, which will briefly be ahead of Airbus when the 737 production rate goes to 47/mo next year, compared with the Airbus plan to take A320 rates to 46/mo next year. The two companies are at parity this year. (Figure 1.)

Summary

- Bombardier, COMAC and Irkut add to supply by 2020, but impact will be minimal.

- No 747-8 deliveries scheduled in 2018. We see program termination coming very soon.

- A330ceo production rate reduced, higher rate for 787 than announced.

- We see short-term Airbus advantage coming in wide-body production rates as A350 ramps up. We stick with our call that 777 Classic rates have to come down.

- We reduce A380 production rates in our estimates.

Redefining the 757 replacement: Requirement for the 225/5000 Sector, Part 2.

By Bjorn Fehrm

Subscription required

Introduction

01 March 2015, c. Leeham Co: In the first part of the article series around the need for a more capable solution for 180-240 seats and 5,000 nautical miles, we went through the derivative aircraft that Boeing could field as competitors to Airbus A321LR and showed why none of them are effective. We also established the market requirements and the likely market size for aircraft that shall cover this segment and the required efficiency and overall cost improvement needed.

We will now look at different solutions to the requirements, first by analyzing what key characteristics does single and dual aisle aircraft have and what consequences will they have for the aircraft’s efficiency parameters like weight, size and drag. Once we have these characteristics we can design adapted aircraft types and calculate their economics such as fuel costs and other costs and we can also establish their operational ground handling times and thereby the consequences single or dual aisle will have on the aircraft utilization.

Having developed and presented these facts it will be possible to forecast what will be the most likely results of Boeing’s New Airplane Study, NAS that we presented 2 November last year. Boeing now uses the name, Middle of the Market (MOM) in place of the NAS.

Summary:

Our second article shows:

- Drag and weight per seat for today’s short and mid-range aircraft vary significantly between single and dual aisle aircraft

- There is a strong correlation between aircraft wetted area and aircraft weight.

- Dual aisle designs in the 180-240 seat segment will have to be highly optimized to be able to compete with single aisle, if at all.

Boeing’s dedicated freighters views an improving market

Subscription Required

By Scott Hamilton and Bjorn Fehrm

Introduction

Feb. 22, 2015: An improving global freight market gives Boeing hope that air cargo demand will support the production of two new main-deck freighters a month for years to come. Boeing is struggling to sell 747-8Fs to keep the 747 line alive and needs to sell the 777F to support its goal of maintaining the current 777 production rate of 100/yr through the transition in 2020 to the new 777X.

Randy Tinseth, VP Marketing for Boeing included the projection as a passing reference in remarks Feb. 11 to the 14th Annual Conference of the Pacific Northwest Aerospace Alliance in Lynnwood (WA). The following week we spoke at length with Tom Crabtree, Boeing’s Regional Director, Airline Market Analysis, Marketing & Business Development, about the long-suffering global cargo market and Boeing’s forecast for recovery.

Summary

- Increasing reliance on belly capacity doesn’t negate need for large main deck freighters, Boeing says.

- Boeing sees need for two new-build, large freighters per month.

- Accepting Boeing’s demand forecast, Leeham Co. sees another production rate cut for the 747-8.

Bombardier’s crisis of confidence perhaps the biggest challenge for CSeries

Subscription Required

Introduction

Feb. 18, 2015, c. Leeham Co.: Alain Bellemare, Bombardier’s new president and chief executive officer, has his work cut out for him.

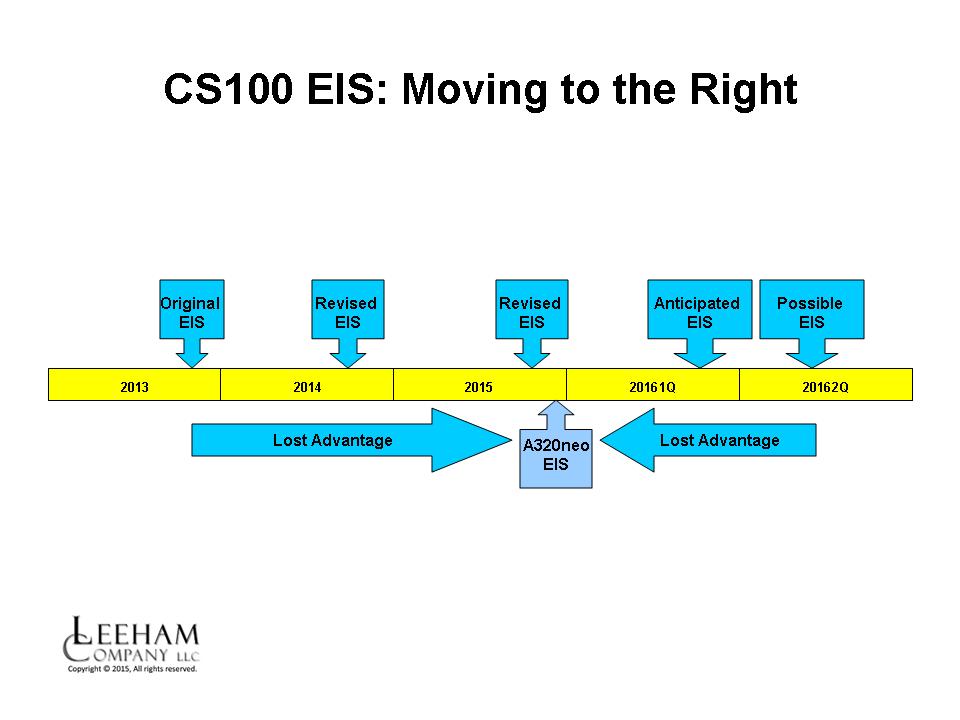

Figure 1. The CSeries was supposed to enter service in late 2013, two full years ahead of the Airbus A320neo. This market advantage has been lost with repeated delays. BBD is sticking to its public statement that EIS is now the second half of this year (most put EIS in the fourth quarter), but there is growing belief EIS will slip to the first or even the second quarter of next year–after the A320neo EIS. Source: Bombardier, Airbus, Leeham Co. Click on image to enlarge into a crisp view.

We outlined the corporate and market perception challenges ahead of him in our Feb. 13 post. Investor and media reception to the CEO leadership change was mixed. Although Bellemare’s appointment was seen as a positive, stock traded down and Bombardier took a pounding in the press (see some reaction at the bottom of this post).

He also has challenges with a changing market place, driven by two years worth of delays in the CSeries program and exacerbated by a changing global political environment.

Summary

- Bombardier faces a crisis in confidence from customers that has to be fixed.

- The CSeries has lost its entry-into-service advantage over the Airbus A320neo and has reduced its advantage over the A319neo, the Boeing 737-8/7 and Embraer E-190/195 E2 EIS due to delays.

- A changing global political environment poses additional risks to the CSeries skyline.

Regional operations with the Turboprop, propjet or Jet; Part 2.

By Bjorn Fehrm

Subscription required

Introduction

15 Feb 2015: In Part 1 of this article series we started comparing the alternatives available for turboprop short haul services in the 70 seat segment; ATR72-600 and Bombardier Q400. We also included the closest regional jet, CRJ700 from Bombardier, to compare costs and see where a jet would be ![]() needed to keep trip times within reason.

needed to keep trip times within reason.

In Part 1 we went through the capacity of the aircraft and their basic characteristics. We also did a first check of their typical fuel consumption on a standard mission of 300 nautical miles.

We will now look closer at the economics of the aircraft; we fly them over different sectors with different speed profiles. We will also dissect their Cash Operating Costs (COC) and Direct Operating Cost (DOC). Having done all this we will look at the crossover points; for what market is ATR72 the choice and where does Q400 fit. And finally, what route sectors require a jet?

Summary:

- The ATR72-600, Bombardier Q400 and CRJ700 are quite different aircraft. The monikers turboprop, “propjet” and jet fit them well.

- The positioning of the end of the scale products are clear, the intriguing aircraft is the Q400. When does it makes sense and has Bombardier positioned it correctly?

- How does one explain its recent meager sales? Wrong aircraft at wrong time? Weak sales force? Wrong markets?

Redefining the 757 replacement: Requirement for the 225/5000 Sector

By Bjorn Fehrm

Subscription required

Introduction

25 Feb 2015: Speculation continues to ramp up during the last weeks and months about what Boeing is up to in the 180 to 250 seat sector and what might be Airbus’ response on top of the A321LR. The segment is not well covered today within production aircraft where 737-900ER and the forthcoming MAX 9 cover up to 210 seats and A321-200 and A321neo up to 220 seats. Both fly their passengers up to a realistic mission of 3000nm, i.e. transcontinental USA.

The next in production aircraft are 787-8 and A330-200 at 240 to 280 seats. These are long range dual aisle aircraft with empty weights more than double of the former pair. The 787-8 and A330-200 per seat economics on shorter missions are therefore in another ball game.

The only aircraft that currently bridges this gap is the out-of-production Boeing 757 and there has been much debate how this shall be replaced. We have covered this question in a number or articles focusing on in turn:

We also covered the study work underway at Boeing to cover this segment. We will now dig deeper into this corner after Boeing has unequivocally stated it does not see a re-engine 757 covering this segment and any aircraft that the airlines want should be a bit larger than the 757.

Summary:

Over a series of articles we will cover:

Read more

Leave a Comment

Posted on February 25, 2015 by Bjorn Fehrm

Airbus, Airlines, American Airlines, Boeing, GE Aviation, Leeham News and Comment, Premium

737 MAX, 747-8, 757, 787, Airbus, Boeing, KC-767