Leeham News and Analysis

There's more to real news than a news release.

Boeing 777-300ER and its replacements; A350-1000 and 777-9X.

By Bjorn Fehrm

Subscription required.

Introduction

Dec. 21, 2014: Last week we did a deep analysis of A380 and its competition. It has been windy weeks for the aircraft since the Airbus Global Investor Forum and it was time to bring some needed facts on the table. These facts showed there is a clear difference between the hype being perpetuated in the media and the reality. As we cleared the situation around the A380, we also touched on the large twins that could fulfill at least parts of its missions.

![]() There has been a lot of discussion around these aircraft as well as they form the battle of titans one level down from A380, the large, long-haul market today dominated by Boeing’s 777-300ER (the A380 does not have a real competitor–the 748i is clearly smaller, in fact so much smaller that it will be engulfed by the 777-9X).

There has been a lot of discussion around these aircraft as well as they form the battle of titans one level down from A380, the large, long-haul market today dominated by Boeing’s 777-300ER (the A380 does not have a real competitor–the 748i is clearly smaller, in fact so much smaller that it will be engulfed by the 777-9X).

Summary

- The 777-300ER had an exclusive run in its size until launch of the A350-1000;

- The A350-1000 doesn’t enter service until 2017;

- 777-9 EIS set for 2020, with hopes to advance by six months;

- We undertake a full economic analysis which gives good cues as to the future dominance of Boeing or Airbus in this highest margin segment of the market.

A380, a deep analysis of its competitiveness

By Bjorn Fehrm

Subscription required.

Introduction

Dec. 18, 2014: In our Monday article we go behind the scenes of the doubts that were spread over the A380 by Airbus last week. To complete the picture we now update our competitive analysis that we did in February this year. We then compared the A380 to Boeing’s 747-8i, the 777-300ER and the forthcoming 777-9X. We also included Airbus closest aircraft, the A350-1000.

![]() A lot has happened since then. Airbus has done a lot of work on the passenger area of the A380 to offer increased passenger densities and the pictures of the emerging Boeing 777-9X and Airbus A350-1000 is now clearer.

A lot has happened since then. Airbus has done a lot of work on the passenger area of the A380 to offer increased passenger densities and the pictures of the emerging Boeing 777-9X and Airbus A350-1000 is now clearer.

Sales efforts of the A380 has also progressed, with meager results despite adding a leasing proposition what should make the hurdles of operating a small sub-fleet of A380s lower. To understand why, we interviewed Mark Lapidus, the CEO of Amedeo, the leasing company which specializes in financing and leasing of A380s. We wanted specifically to talk to Lapidus about the reactions of the airlines to the A380 and what problems he saw in selling an aircraft of this type.

In preparing the article we also gathered additional info from Airbus and Boeing, from the former around their work on the cabin configurations and densities, from the latter the maintenance costs for the up and coming 777-9X.

Summary

- In our February article we established that an A380 is roughly equal on fuel per passenger transported to the benchmark in the present non-VLA long haul market, the Boeing 777-300ER. We also found that this is highly dependent on how many passengers one assumes for both aircraft in the comparison.

- We could also see that come 2020, when the replacement of the 777-300ER would be available, the 777-9X, A380 would trail with up to 20% in fuel efficiency, once again dependent on how many seats were used in the comparison.

- At the time we only looked at a fuel consumption comparison; we did not include crew cost, maintenance costs, landing and en route fees to generate Cash Operating Costs (COC) or capital costs to come to Direct Operating Cost (DOC). In today’s updated analysis we add these costs items.

- Finally we have talked with Amedeos CEO Mark Lapidus, asking about his discussions with the Airline CEOs and their teams, to understand what the reactions are from the airlines and why has he not placed any A380 with customers yet.

As we did this deeper study, a more nuanced and different picture emerged from the one seen in February. The results busts a number of deeply engraved myths, one being that four engines are more expensive to fly and maintain than two.

Lufthansa to use A340s in “lower cost” operation; our analysis against the 787

Subscription required.

By Scott Hamilton and Bjorn Fehrm

Introduction

Low cost long haul service is gaining traction, but previous efforts proved difficult to be successful.

Dating all the way back to Laker Airways’ Skytrain and the original PeoplExpress across the Atlantic, airlines found it challenging to make money.

More recently, AirAsiaX retracted some of its long-haul service, withdrawing Airbus A340-300 aircraft when they proved too costly. The airline recast its model around Airbus A330-300s as an interim measure, unable to fly the same distances as the longer-legged A340. AirAsiaX ordered the Airbus A350-900 and now is a launch customer for the A330-900neo.

![]() Cebu Pacific of the Philippines is flying LCC A330-300 service to the Middle East. Norwegian Air Shuttle famously built its entire LCC long haul model around the Boeing 787, initiating service with the 787-8 and planning to move to the 787-9.

Cebu Pacific of the Philippines is flying LCC A330-300 service to the Middle East. Norwegian Air Shuttle famously built its entire LCC long haul model around the Boeing 787, initiating service with the 787-8 and planning to move to the 787-9.

Canada’s WestJet is leasing in four used Boeing 767-300ERs to offer LCC service,

Legacy carrier Lufthansa Airlines plans to use fully depreciated A340-300s to begin “lower cost” (as opposed to “low cost”) long haul service. LH says the fully depreciated A340s come within 1%-2% of the cost per available seat mile of the new, high capital-cost 787s.

Summary

- AirAsiaX’s A340 LCC long haul service proved unprofitable. Can Lufthansa’s similar service with fully depreciated A340s work?

- Our analysis shows that it can. It can even support the lease rates that would be charged for a 10 year old A340 if the fuel price remains at the present level.

- When doing the research for this article and going through the results of our proprietary model we started to ask ourselves, is the A340-300 the ugly duckling of the airline market?

Odds and Ends: 787 donation; Alenia sues Bombardier over CSeries; 2016 777 delivery slots opening up

787 donation: The Boeing Co. handed over 787 test airplane #3 (ZA003) to the Museum of Flight Saturday in an elaborate ceremony marking an unprecedented donation of a modern airliner to an aviation museum.

Boeing 787 ZA003, which went on a world sales tour, was donated to Seattle’s Museum of Flight Nov. 8, 2014. The logos of customers bracket the #2 door. Photo by Leeham News and Comment. click to enlage.

To be sure, the donation was made possible by the fact that ZA003 (and 002 and 001) can’t be sold due to the massive rework necessary, and these three airplanes have been written off for more than $2bn. But this doesn’t make the event any less significant.

Airbus poised to overtake Boeing in wide-body sector, bracket Boeing at both ends

Subscription required.

Introduction

Airbus is poised to produce more medium twin-aisle airplanes than Boeing by the end of 2017 and maintain ![]() the lead into the early 2020 decade, according to production rates that have been announced, unannounced and based on estimates according to production gaps; and other information, a Leeham News and Comment analysis shows.

the lead into the early 2020 decade, according to production rates that have been announced, unannounced and based on estimates according to production gaps; and other information, a Leeham News and Comment analysis shows.

The wide-body arena has traditionally been Boeing’s to dominate. Although Airbus has outsold Boeing in this sector in recent years, Boeing’s greater production capacity and earlier-to-market 787 vis-à-vis the A350, which will only deliver to its first operator next month, maintained the advantage for Boeing’s market share for years.

The A340 wasn’t a high-demand airplane, eclipsed as it was by emerging ETOPS authority and a highly desirable, very efficient 777 Series.

Airbus and Boeing each face challenges with their aging wide-bodies. The 777 Classic is now on its downward life cycle following the launch of the re-engined, re-winged 777X. Boeing claims it can maintain current production rates of the Classic, but the official line is about the only one that believes this.

Airbus’ A330 Classic, now called the ceo after the launch of the A330neo program, similarly was headed toward sharp declines in the production rates. Airbus quickly achieved 121 commitments for the neo, but first delivery isn’t planned until December 2017 (which probably means 1Q2018) and it still needs to bolster the backlog of the ceo, which drops sharply in 2016. Airbus has been far more transparent than Boeing about the risk to the production rate, and announced a reduction from 10/mo to 9/mo in 4Q2015. We don’t think this will be enough, and Airbus has talked about rates of 7-8/mo.

With this as a backdrop, we believe Airbus will begin out-producing Boeing in medium-wide-bodies within a few years. We leave out the Very Large Aircraft as highly niche. But inclusion would only make the case worse for Boeing. We expect the 747-8 production rate to be cut from 1.5/mo to 1/mo, with an announcement coming as early as next month. Airbus is currently producing the A380 at 2.5/mo.

Summary

- We forecast the crossover point in production favoring Airbus in 2017.

Airbus has notified the supply chain to plan for a higher-than-announced rate of 10/mo for the A350. - We expect the A330ceo rate to be further reduced, offset by the ramp-up of the A330neo.

- We expect the 777 rate to begin falling in 2017 and continue to fall up to the EIS of the 777X in 2020.

- Ramp up of the 777X rate will take several years, providing Airbus a production rate advantage from 2017 through at least 2022.

- Airbus already has the advantage over Boeing in the single aisle sector. Gaining the advantage over Boeing in the twin aisle sector brackets Boeing in a way that has never been done before.

Boeing considers single, twin aisle, co-development 757/767 style for next new airplane

Subscription required.

Now open to all Readers.

Introduction

Boeing is looking at a number of scenarios for its New Airplane Study (NAS) that would replace the 757 and 737, have ranges from 4,000nm-5,000nm, and carry as few passengers as 130 or as many as 240.

![]() To cover this broad range of demands could require reverting back to the 1980s when Boeing simultaneously developed two airplanes serving very different missions, the 757 and 767, that shared cockpits and some other common elements.

To cover this broad range of demands could require reverting back to the 1980s when Boeing simultaneously developed two airplanes serving very different missions, the 757 and 767, that shared cockpits and some other common elements.

Boeing faces some hard decisions in the coming years, as Airbus outflanks Boeing in the single-aisle sector with the A320neo family and its latest offering, the A321neoLR. Our analysis and sales figures show the 737 MAX falling further and further behind in market share as MAX 9 lags vis-à-vis the A321neo.

We spoke with Kourosh Hadi, director of product development at Boeing, during a break at a conference last week organized by the British American Business Council-Pacific Northwest, and covered this and a number of other topics.

Summary

- Boeing is studying a New Light Twin (NLT) and New Single Aisle (NSA) to replace the 757 and 737 airplanes.

- The tipping point between an efficient NSA and the NLT is around the passenger size of the 757-200.

- Boeing is evaluating materials, including metals and composites, for the NAS and the manufacturing process, which will also be a determining factor in the materials for the new airplane.

- Engine advances for the 777X’s GE9X are beyond the GEnx and CFM LEAP of today and could help drive the next new small engine technology.

- Although having a miniscule portion of the 100-150 seat market, Boeing today plans to continue participation in at least the 130 or 150 seat sector even as airplane size moves up every year.

Part 3: Boeing 757 replacement: 757 and Airbus A321neoLR versus clean sheet designs.

Subscription required.

By Bjorn Fehrm

Part 3 of 3

Introduction

In Part 2 of our three-part 757 Replacement analysis, we took a close look at Airbus’ new 97 tonne take-off weight A321neo, revealed in a world exclusive by ![]() Leeham News and Comment October 21. We analyzed the A321neoLR’s capabilities and limitations when compared to Boeing 757-200W and we saw that it could do the international flights that the 757-200 does with about 25% better efficiency. In this final Part 3, we will now compare the 757 and A321neoLR against what can be Boeing’s reaction, a clean sheet New Single Aisle, NSA, or New Light Twin Aisle, (NLT). First the conclusions from Part 2:

Leeham News and Comment October 21. We analyzed the A321neoLR’s capabilities and limitations when compared to Boeing 757-200W and we saw that it could do the international flights that the 757-200 does with about 25% better efficiency. In this final Part 3, we will now compare the 757 and A321neoLR against what can be Boeing’s reaction, a clean sheet New Single Aisle, NSA, or New Light Twin Aisle, (NLT). First the conclusions from Part 2:

- When using the United Airlines-configured 757-200W international as benchmark, we came within seven seats of the 757 capacity for an A321neoLR. It covered the same range and had trip fuel costs that were 25% lower.

- The per seat fuel costs gave a 22% higher efficiency, which was within 2% of Airbus own figures.

- 737 MAX9 is not suitable for stretch to an international version, not because the wing is not good enough but because the MAX9 cannot bring the wing to an angle at take-off where it can work efficiently; the landing gear is too short.

Summary

For Part 3 we can summarize:

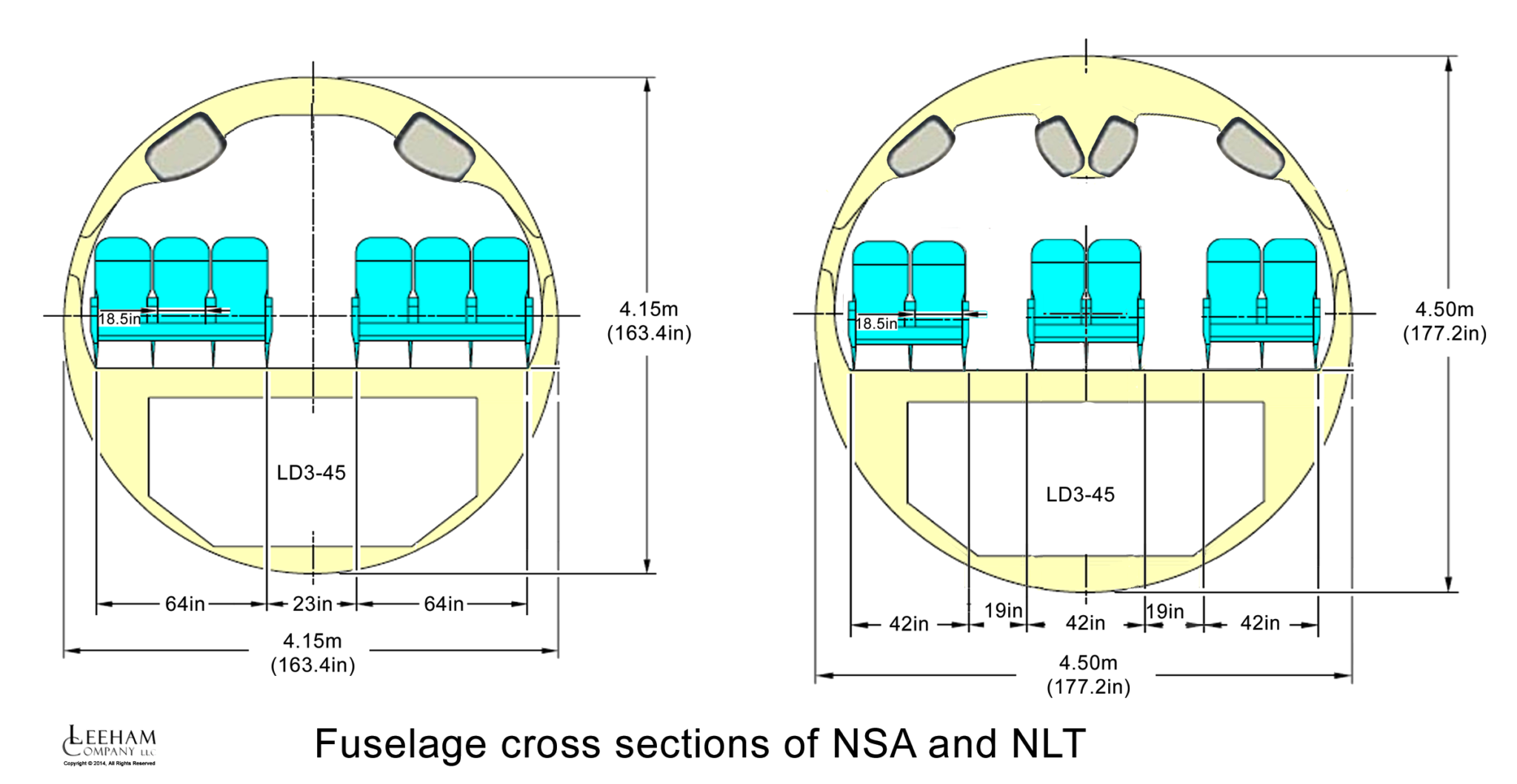

- A New Single Aisle (NSA) or New Light Twin (NLT) which would enter the market in 2025 would be sized at around 200 passengers with subsequent variants covering the 175-225 seat market, all numbers with OEM standard two-class seating. Figure 1 shows the fuselage cross sections we have used in our modelling of NSA and NLT to cover this market segment.

Figure 1. Fuselage cross sections of our models of NSA and NLT. Source: Leeham Co.

- In order to cover the market segment of the 737, A320 and 757 it would have a range in excess of 4,100nm. We will use 4100nm for our modeling to maximize the comparative efficiency information.

- Its efficiency would be higher than an A321neoLR, primarily due to better engines and a more modern wing.

- The New Light Twin (NLT) wins on comfort and ground turn-around time but pays with a larger fuselage cross section due to the extra aisle. This causes more drag and structural weight, net effect is a reduction in efficiency of around 2.5%.

Boeing 737 MAX 8 as a long and thin aircraft and how it fares in general versus Airbus A320neo.

Subscription required.

By Bjorn Fehrm

Introduction

Over the last weeks we have looked at Boeing’s 757 replacement possibilities on its long and thin network niche, including a ground breaking launch interview for the A321neoLR with Airbus Head of Strategy and Marketing, Kiran Rao. In the series we have seen that the A321neo has the potential to replace the 757-200 on long and thin international routes. Boeing’s equivalent single aisle entry, 737 MAX 9, has problems to extend its range over 3,600nm. It is too limited in the weight increase necessary to cover the longer range.

Marketing, Kiran Rao. In the series we have seen that the A321neo has the potential to replace the 757-200 on long and thin international routes. Boeing’s equivalent single aisle entry, 737 MAX 9, has problems to extend its range over 3,600nm. It is too limited in the weight increase necessary to cover the longer range.

Many have asked how the less- restricted Boeing 737 MAX 8 would fare, suitably equipped with the necessary extra tanks. This is the subject of this week’s sequel on the theme long and thin. At the same time we look at Airbus entry in this segment, the A320neo, to see how it stacks up to the 737 MAX 8, both in their normal 1,000 to 2,000nm operation and then also in a long and thin scenario.

Let’s first summarize what we found so far in our four articles around the Boeing 757 and its alternatives:

Summary

Figure 1. Boeing 737 MAX 8 overlaid with Airbus A320neo. Source: Leeham Co.

Read more

4 Comments

Posted on November 9, 2014 by Bjorn Fehrm

Airbus, Airlines, Boeing, CFM, GE Aviation, Leeham Co., Leeham News and Comment, Pratt & Whitney, Premium, Rolls-Royce

737, 737 MAX, 737NG, A320, A320NEO, Airbus, Boeing, CFM, Pratt & Whitney, Rolls-Royce