Leeham News and Analysis

There's more to real news than a news release.

Pontifications: Embraer, contrary to others, looks to momentum in 2017

By Scott Hamilton

Jan. 3, 2017, © Leeham Co.: Airbus, Boeing and Bombardier look toward 2017 as a bit of a punk year, as detailed in our Look Ahead for subscribers only. Not so by Embraer.

In an exclusive interview, John Slattery, the president of Embraer Commercial, said EMB will gain “momentum” this year. This is at a time where sales at the other three of the Big Four OEMs are expected to slow off an already slow 2016.

Seventeen new, derivative aircraft to see EIS through 2020

Subscription Required

Introduction

Delivery of the first Bombardier CS300, to AirBaltic, next week kicks off entry-into-service for 17 airplanes through 2020. Bombardier photo.

Oct. 20, 2016, © Leeham Co.: The past decade was a hive of activity as the Big Four OEMs launched new airplane programs and put the aircraft into service.

Airbus launched the A320neo, A330neo and A350 families. The A330neo is under production; the other two entered service early this year.

Boeing launched the 787 in late 2003 (outside the decade mark), rolled it out in 2007 and entered service with it in 2013. The 737 MAX was launched in 2011 and is in flight testing. The 777X was launched in 2013; components are in production.

Bombardier launched the CSeries in 2008; it entered service this year, after three years of delays.

Embraer launched the E-Jet E2 om 2013. Flight testing began this year.

New Entrants

These were supplemented by new entrants into commercial aviation: COMAC with its C919; Irkut with the MC-21; and Mitsubishi with the MRJ90. Of these, only the MRJ90 is flying. After more than two years of delays and several false starts, flight testing began in earnest this week at Moses Lake (WA) with FTA-1 (Flight Test Aircraft 1).

Development and new program launches have slowed, but the next decade is hardly going to be idle.

Summary

- Seventeen new aircraft or derivatives are scheduled to enter service through 2020.

- Five potential derivatives might see EIS through the same period.

- Three to five new or potential derivative aircraft might see EIS 2021-2025.

Airline assets and lessor assets: Bombardier and Embraer

Subscription Required

Part 2. Part 1 may be found here.

Introduction

Bombardier invented the regional jet. Despite some sales these days, the CRJ was eclipsed by the Embraer J-Jet. Bombardier photo.

Oct. 10, 2016, © Leeham Co.: Regional aircraft are much riskier assets for lessors than mainline aircraft.

Until recently, Bombardier and Embraer were the only two regional jet Original Equipment Manufacturers (OEMs).

Today, the Sukhoi SSJ100 and the Mitsubishi MRJ90 join BBD and EMB in this arena.

Summary

- Bombardier’s regional jets CRJ series enjoyed a good life with airlines and lessors, but fell into disfavor as fuel prices spiked.

- BBD’s CSeries was ordered by four lessors, but two of them have question marks.

- Embraer’s E-Jet found good homes with lessors, but some worry about supply-and-demand in the secondary market.

Bjorn’s Corner: The Chinese aircraft engine industry

By Bjorn Fehrm

October 07, 2016, ©. Leeham Co: In our Corners on East bloc aeronautical industries, we will now look at the Chinese civil aircraft engine industry.

The Chinese engine industry is closely modeled after the Chinese aircraft industry that we looked at last week. It is organized as divisions and later subsidiaries to the major aircraft companies. Contrary to the Chinese aircraft industry, it has had major problems in gaining the necessary know-how to start developing and producing its own designs.

The industry has built Soviet designs on license since the 1950s and only recently managed to present functional own designs, after many failures.

Bjorn’s Corner; The Russian civil aircraft engine companies

By Bjorn Fehrm

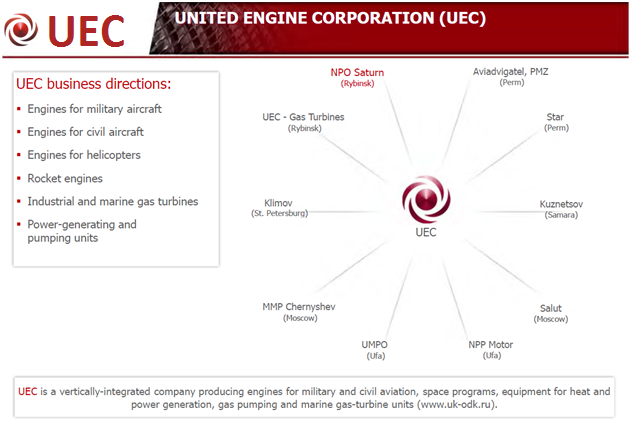

September 23, 2016, ©. Leeham Co: In our Corners on East bloc aeronautical industries, we now look at the main Russian civil aircraft engine companies. As with the aircraft side, there is one overall Russian engine company since 2008, United Engine Corporation (UEC), Figure 1.

This is a state-owned holding which incorporates 80%of the gas turbine engine companies from the Soviet times, employing 80,000 people.

The aim is to coordinate and optimize Russia’s engineering and production resources around present and future gas turbine engines for Aeronautical, Naval and Stationary use.

Figure 1. Engine companies in United Engine Corporation. Source: UEC.

Soviet and Russian engines have historically been named after their chief designer in the design bureau. We will now describe the main entities in UEC that work with airliner engines. Read more

Bjorn’s Corner; The Russian civil aircraft companies

September 16, 2016, ©. Leeham Co: In our Corners on East bloc aeronautical industries, we will now look at the main Russian civil aircraft companies. There is one overall company since 2006, United Aircraft Corporation (UAC).

This is a state-owned holding which incorporates 30 of the main companies from the Soviet times, employing 100,000 people. The aim is to coordinate and optimize Russia’s project and production resources around the present aircraft and the future projects that Russia can afford to drive.

Figure 1. Map of UAC Companies in Russia outside of Moscow region. Red markers are MRO. Source: UAC.

UAC consolidates several company groups that were formed after the fall of the Soviet Union 1990 and up to the formation of UAC in February 2006.

We will now dissect the main UAC groups and companies that are involved in civil aircraft development and production. Read more

Bjorn’s Corner: East bloc aeronautical industries

By Bjorn Fehrm

September 09, 2016, ©. Leeham Co: The Western world civil aeronautical industry developed a number of new aircraft (Boeing 787, Airbus A350, Bombardier CSeries, Mitsubishi’s MRJ) or aircraft variants (A320neo, 737 MAX, A330neo, Embraer’s E-Jet E2) during the last 15 years. The last of these projects (A330neo) is entering flight tests within six months.

Figure 1. The MC-21 project is reviving the Russian aeronautical industry. Source: UAC.

Over the next 10 years there will be few new Western hemisphere aircraft projects. But there will be action in the east, in Russia and China. We therefore will cover these projects in more and more articles.

To give a background to these articles, I will spend some Corners to describe some of the differences between the Western and Eastern aeronautical industry. A lot of these differences will come from the industry’s history. We will start with Russia’s airframe industry. Read more

2017: the year ahead

Subscription Required

Introduction

Jan. 3, 2017, © Leeham Co.: The New Year is here and it doesn’t look like a good one for commercial aerospace, if measured against previous outstanding years.

There are some troubling signs ahead, piling on to a slowdown in orders from last year that didn’t even reach a 1:1 book:bill.

This year looks to be worse than last. Airbus and Boeing will give their 2017 guidance on the earnings calls this month and next. Bombardier and Embraer earnings calls are a ways off, when each will provide its guidance.

But LNC believes the Big Two in particular will be hard pressed to hit a 1:1 book:bill this year and may even struggle to match 2016 sales.

Boeing’s year-end order tally comes Thursday. Airbus’ comes on Jan. 11.

Summary

Read more

1 Comment

Posted on January 3, 2017 by Scott Hamilton

Airbus, ATR, Boeing, Bombardier, CFM, Comac, CSeries, E-Jet, Embraer, Etihad Airways, Farnborough Air Show, GE Aviation, Irkut, Leeham News and Comment, Middle of the Market, Mitsubishi, Pratt & Whitney, Premium, Rolls-Royce, Sukhoi

Airbus, Boeing, Bombardier, CFM, Comac, Embraer, GE Aviation, Irkut, Mitsubishi, Pratt & Whitney, Rolls-Royce, Sukhoi