Leeham News and Analysis

There's more to real news than a news release.

CFM LEAP accelerating in test program; Airbus and the A350-800

Aviation Week has a long, detailed story about the test program for the CFM LEAP engine, which is accelerating rapidly.

In its 737 MAX program update yesterday, Boeing said the LEAP-1B has begun testing and it will benefit from the testing already underway for the LEAP-1A, the version that is designed for the Airbus A320neo family. The LEAP-1C for the COMAC C919 is on its original schedule for certification in 2015, despite the fact the C919 has slipped to at least 2017, reports AvWeek.

The 737 MAX is exclusively powered by the LEAP, as is the C919. The former has more than 1,600 firm orders and the latter just hit its 400th order/commitment. CFM faces competition on the A320neo family from Pratt & Whitney’s P1000G Geared Turbo Fan, where PW holds a 49% market share against CFM, which previously held a larger, more dominate position in the A320ceo competition. A large number of orders don’t yet have an engine selection.

PW is the sole-source engine provider for the Bombardier CSeries, the Mitsubishi MRJ and the Embraer E-Jet E2. PW splits the engine choice on the Irkut MC-21 (soon to be renamed the YAK 242) with a Russian engine.

Just as Boeing’s LEAP-1B will benefit from the experience of the LEAP-1A now in testing for Airbus, Airbus will benefit from the testing and experience of PW’s testing of the GTF on the Bombardier CSeries.

Aviation Week also has a story about the Airbus A350-800 with the blunt headline, The airplane Airbus doesn’t want to build. This refers to the A350-800. AvWeek muses that the outcome of the merger between US Airways, now the largest customer for the airplane, and American Airlines, may be the deciding factor for the airplane. We agree. With American’s large order for the Boeing 787-9, the A350-800 would be unnecessary.

That would then leave Hawaiian Airlines as a key decision-maker. We hear in the market that Hawaiian is just sitting back and waiting to see what kind of incentives Airbus will offer to entice a switch to the larger A350-900.

Is tide ready to turn for CSeries?

CS100 first flight, September 16, 2013. Photo via Seattle Times.

Is the tide ready to turn for the Bombardier CSeries?

Following a nine month delay, the CS100 Flight Test Vehicle #1 took to the air September 16. It’s flown only twice since and has been undergoing ground vibration tests and more software upgrades. BBD is pretty mum about the testing program, which causes speculation about whether some issue emerged during the three flight tests. But we’re told by a source familiar with the program, but who is not with BBD, that BBD is being conservative in its pace, counting on the fact that it will eventually have seven FTVs to bring entry-into-service on time. A few Canadian aerospace analysts think EIS will slip to 1Q2015.

Then there are the orders, just 177 firm, which is more than those for the Airbus A319neo and the Boeing 737-7 MAX combined, but which the market perceives as low and a slow-selling program. Bombardier points out that the firm sales are about on par with other new airplane programs at this stage, but the market–dazzled by the thousands of orders placed for the NEO and MAX–won’t make these distinctions.

But it’s possible the tide is ready to turn for the CSeries. Here’s why.

- Potential customers have been waiting for the first flight and to see whether the program will be more or less on time with the new, implied schedule emanating from first flight. We believe a few more months have to pass before any conclusions are drawn on this score.

- Likewise, a few months have to pass before Bombardier and Pratt & Whitney will know whether the economic promises will in fact be achieved.

- There are some key sales campaigns for which decisions should be made in the coming months, both this year and into next, that if BBD wins will serve to build significant momentum.

- Airbus is running out of delivery slots for the entire A320 family. The VivaAerobus order announced October 21 includes deliveries beginning next year. The backlog goes to 2019-2020, and while John Leahy, COO-Customers, is adept at finding slots through juggling the skyline, there simply aren’t too many left mid-term. Bombardier is sold out into 2016 and is a better position to offer deliveries in quantity. This makes it difficult for Leahy to “buy” a deal, which he has done on several occasions, to under-price CSeries to a point where BBD can’t play in the sandbox.

- Boeing remains more focused on the 737-8/9 than on the 737-7, leaving BBD to largely fight its war against the diminishing Airbus and the forthcoming Embraer E-190/195 E2, the latter with a planned EIS of 2018, a good three years after CS100 enters service.

It will likely be next year before solid trends are noticeable. BBD retains its goal of reaching 300 firm orders and 20-30 customers by EIS, at least a year from now. We think this is easily achievable.

Update, Oct. 22: The Iraq-Business News reports that the government has approved the purchase of five CS300s at $40m each.

Odds and Ends: Embraer reports weak quarter; MRJ FTV #1 assembly; JAL, ANA politics

Embraer’s Third Quarter: Embraer delivered fewer commercial airplanes in the third quarter than had been expected. The maker of E-Jets and the E-Jet E2 re-engined versions due beginning in 2018 listed its deliveries and backlog in its press release. Analysts expects 22 E-Jets would be delivered in the quarter. But the backlog is up 44% year-over-year, largely on the strength of the launch of the E2 (150 orders, 100 of which are for the smallest E-175 E2 and 25 each for the E-190/195 E2), and orders from Republic Airways Holdings and SkyWest Airlines for the current generation of E-Jets. The E-175 remains to most frequently-ordered airplane.

Although Embraer is expanding the size of the E-195-E2 by up to 12 seats, orders have been few. The E-190 has proved a better-selling model than the E-195.

Source: Embraer

Officials expect to have a healthy fourth quarter delivery stream.

Mitsubishi MRJ: Assembly for the first Mitsubishi MRJ Flight Test Vehicle (to borrow Bombardier’s term for the CSeries) is underway. The first delivery was originally planned for this year; it’s now planned for 2017, four years late. This rivals Boeing’s 787 and exceeds the Airbus A350 and as yet the CSeries.

JAL, ANA Politics: Reuters has an analysis about the suspicion politics may have been involved in the decision by Japan Airlines to buy the Airbus A350 and the pending order by ANA of an Airbus or Boeing airplane.

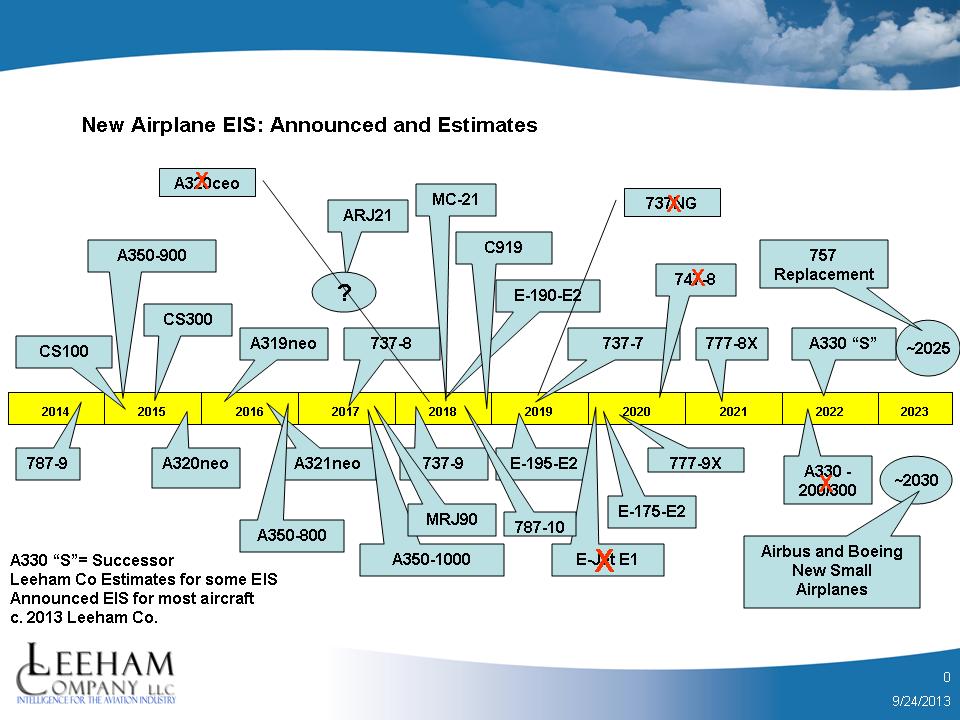

Busy decade ahead for new, derivative airplane EIS dates

The next decade will see an extraordinary number of new and derivative airplanes entering service, beginning next year with the Boeing 787-9 and ending in 2022 with what we believe will be a replacement for the Airbus A330.

Bombardier’s CS100 is currently planned to enter service in around September next year, 12 months after its first flight on September 16, 2013, but we think EIS will slip to early 2015. Bombardier seems to be laying the groundwork for this in statements that it will reassess the EIS date in a few months.

Beginning with the 787-9, there is a steady stream of EIS dates–and a couple of end-production dates of current generation airplanes.

This chart captures the airplanes and their dates. Most dates are based on firm announcements from the OEMs, but we’ve adjusted some based on market intelligence and our own estimates.

.

The arrows to certain points within years are not necessarily representative of specific timelines within that year. OEMs generally are not too specific about and EIS date, preferring to say “first half” or “second half” or some derivative of ambiguity. The only specific that we’re aware of is Boeing’s revised EIS of the 737 MAX, from 4Q2017 to July 2017. Although the Ascend data base is quite specific, we’ve not attempted to be highly specific in this chart. (Have we been specific enough about all this?)

Readers will note that we have the ARJ21 arrow going to a question mark. This airplane is already seven years late, and supposedly it’s going to enter service next year, but we aren’t banking on this at all. COMAC/AVIC, producer of the ARJ21, has a dismal record of meeting target dates. Accordingly, although COMAC now says the EIS for the C919 is 2017, we’ve got this in 2018–and even this is likely generous.