Leeham News and Analysis

There's more to real news than a news release.

Mitsubishi opens Seattle Engineering Center ahead of MRJ90 first flight

The MRJ90 testing and entry into service timeline. Source: Mitsubishi. Click on image to enlarge.

August 3, 2015, © Leeham Co.: Mitsubishi Aircraft Corp. today opened its Seattle Engineering Center jointly with local company AeroTEC in advance of the first flight of the MRJ90 in September or October. During the second quarter of next year, four of five MRJ Flight Test Vehicles will be domiciled in Moses Lake in Central Washington for the bulk of the flight testing over the following year. Entry into service is planned for 2Q2017 with launch customer All Nippon Airways.

The engineering center represents the first in Washington State for an aircraft OEM other than Boeing. Mitsubishi will assign 50 engineers from Japan to the new SEC, in South Seattle a short distance from Boeing Field. One hundred engineers will be hired locally.

AeroTEC and Mitsubishi began discussing working together only last January, said president Lee Human, who added that the seven months from January to the opening of the SEC today was remarkable for the speed in which negotiations, contracts, permits and hiring was achieved.

LEAP, the best of 1,000 investigated alternatives.

By Bjorn Fehrm

Subscription required.

Introduction

June 23, 2015, © Leeham Co. CFM International went through 1,000 iterations before settling on the final design for the LEAP engines that will power the Airbus A320neo, the Boeing 737 MAX and the COMAC C919.

In an interview with us at the Paris Air Show, CFM LEAP program manager Gareth Richards explained the macro process of the development of LEAP, CFM’s sequel to CFM56. This will be the largest turbofan engine program in the history of civil aviation and the follow on to the world’s most-sold turbofan, the CFM56.

Richards focused on how an engine like LEAP gets designed and what the trades are that a single aisle, short haul engine has compared to long haul engines.

LEAP is sharing the A320neo platform with Pratt & Whitney’s GTF but is sole engine on the 737 MAX and the C919. This will lead to engine production rates five years into the program of 1800 engines which is higher than the present rate of CFM56 deliveries.

Dependant on rate increases by Airbus and Boeing, this can increase beyond 2,000 engines per year after the initial ramp. It would make LEAP the largest civil turbofan program whichever way one counts: engines, installed thrust or revenue.

Summary:

- Research of optimal engine cycle was extensive, with more than 1,000 alternatives investigated before settling on the final LEAP cycle.

- The production ramp is the fastest ever, from 30 engines 2015 to 1,700 by 2019.

- While CFM does not want to ramp faster than planned, final production rate is flexible.

- The large volume of sold engines, the fast production ramp and the short-haul cycle makes for a conservative approach to performance.

- We discuss with Richards how such a program is managed and how you make sure you can deliver on promises.

Bjorn’s Corner: What Paris Air Show taught us about East and West.

By Bjorn Fehrm

25 June 2015, © Leeham Co: With a few days in the office one can look back at Paris Air Show with a bit of perspective. So what are the impressions?

It was surprising how many orders Airbus and Boeing landed. Both had played down the expectations, telling that it will be a decent show but nothing close to record. Yet both were booking orders or commitments which were better than expected going into the PAS. Read more

Airbus COO faces production challenge vs bulging order book

Subscription required.

Now open to all Readers.

Introduction

June 15, 2015, Paris Air Show, c. Leeham Co. Airbus, like Boeing, is faced with an embarrassment of riches: too many  orders for the A320 and A350 production rates that have been announced. There’s pressure from the top commercial officer to hike rates, but the president and chief operating officer says not so fast.

orders for the A320 and A350 production rates that have been announced. There’s pressure from the top commercial officer to hike rates, but the president and chief operating officer says not so fast.

Tom Williams was elevated to the presidency only a few

months ago from his position as EVP-Programs, where he was in charge of production and the Airbus supply chain. Williams, a Scotsman and the first non-French or non-German to be president and COO of Airbus Commercial, ruefully observes he didn’t give up the production and supply chain duties with his new title.

Although Williams agrees with John Leahy, chief operating officer-customers, that demand indicates higher rates are needed for the A320 and A350, the demands on the supply chain for Airbus, as well as the other airframers, also demands caution.

- Summary

- Decision end of this year or early next on A380 production rates.

- A380neo launch aid reported—but it’s premature.

- No decision yet on greater than 50 A320 production rate per month.

- Pondering hike in A350 production rate beyond the 10/mo announced.

- Cabin suppliers a top concern.

Paris Air Show: Qatar and others

Subscription required.

Introduction

June 1, 2015, c. Leeham Co. It could be called the Qatar Airways Air Show.

Qatar Airways plans to have five airliners on display at the Paris Air Show in two weeks: the Airbus A319, A320, A350, A380 and the Boeing 787. The carrier hasn’t  announced whether it will provide an aerial display as it has at previous air shows, but Qatar may well have more airliners there than Airbus or Boeing.

announced whether it will provide an aerial display as it has at previous air shows, but Qatar may well have more airliners there than Airbus or Boeing.

As for manufacturers other than Airbus and Boeing, we don’t expect anything of consequence from these.

Summary

- Irkut, COMAC, Mitsubishi, Sukoi and ATR are other major aircraft producers that will be at the Paris Air Show.

- Engine makers CFM International, GE Aviation, Rolls-Royce, Pratt & Whitney and Engine Alliance will also be there.

- An update on Airbus expectations.

Bombardier CS300 analysis vs A319neo, 737-7

By Bjorn Fehrm

Subscription required

Introduction

March 29, 2015, c. Leeham Co: Bombardier’s big bet in the aeronautics sector, CSeries, is well into flight testing, now more than half way toward the 2,400 hours required by Transport Canada before certification can be granted. The first aircraft to be certified will be the smaller 110 seat CS100 but the market is most interested in the larger 135 seat CS300, which has 63% of present orders and commitments, Figure 1.

Figure 1. Cseries largest model, CS300. Source: Bombardier.

Bombardier’s new CEO, Alan Bellemare, told reporters last week that the CS100 would be certified during 2015 with entry into service slipping into 2016. The CS300, which is a direct challenger to Airbus’ A319neo and Boeing’s 737-7, should follow six months after CS100. With the CS300 in flight testing and going into service next summer, we decided to have a deeper look at CS300 and its competitors.

Summary

- A319 and 737-7 are shrinks of the market’s preferred models, A320 and 737-8, and as such not the most efficient models.

- The CS300 is the series center-point and it shows. The modern design beats the Airbus and Boeing designs on most counts.

- Part of the modern concepts in CSeries is the well-conceived Pratt & Whitney PW1000G geared turbofan.

- PW’s 73 in fan version of the PW1000G for CSeries is slightly less efficient that the 81 in version for A319neo but CS300 lower weight makes sure this is more than compensated for.

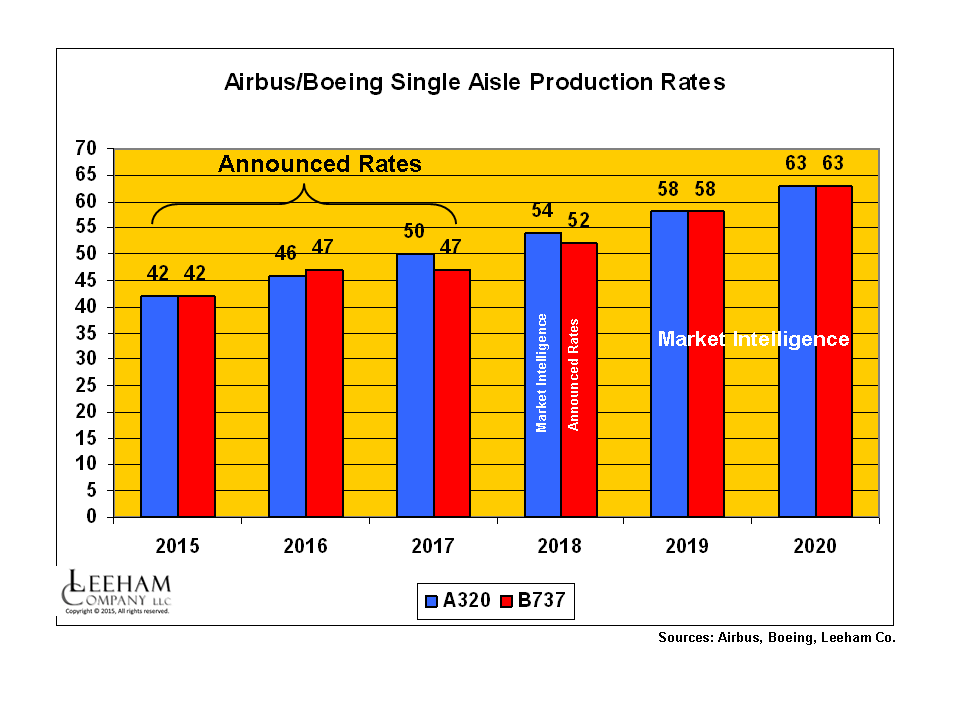

Production rates on single-aisles keep going up, up

Figure 1. Airbus and Boeing production rates for the A320 and 737 lines are going up as announced rates and rates under consideration go to lofty levels. Click on image to enlarge.

Subscription Required

Introduction

March 3, 2015: c. Leeham Co. Production rates for single aisle airplanes continue to go up for the Big Two, following the Airbus announcement last week that the A320 rates will go to 50/mo in 2017 and officials are considering going to more than 60/mo.

We’ve previously reported that Airbus already has notified the supply chain to be prepared to go to 54/mo in 2018.

Rate 50 will propel Airbus ahead of Boeing, which will briefly be ahead of Airbus when the 737 production rate goes to 47/mo next year, compared with the Airbus plan to take A320 rates to 46/mo next year. The two companies are at parity this year. (Figure 1.)

Summary

- Bombardier, COMAC and Irkut add to supply by 2020, but impact will be minimal.

- No 747-8 deliveries scheduled in 2018. We see program termination coming very soon.

- A330ceo production rate reduced, higher rate for 787 than announced.

- We see short-term Airbus advantage coming in wide-body production rates as A350 ramps up. We stick with our call that 777 Classic rates have to come down.

- We reduce A380 production rates in our estimates.

Airbus/Boeing production rates forecast through 2020

Subscription Required.

Introduction

Feb. 3, 2015: Boeing out-delivered Airbus in 2014, for the second year in a row, as the 787 program improved in delivery rates and before the A350 made its first delivery in December.

Topping Airbus in deliveries allowed Boeing to claim it is the world’s leading ![]() commercial airplane manufacturer. By the delivery metric, Boeing is. By orders, Airbus came in first again, maintaining a decade-long lead.

commercial airplane manufacturer. By the delivery metric, Boeing is. By orders, Airbus came in first again, maintaining a decade-long lead.

The A350 ramps up its production this year even as the A330ceo rate begins to come down at the end of the year and further next year. Boeing vows to maintain the current production rate of the 777 Classic at 100/yr. The 747-8 rate is declining. And both companies are ramping up rates of the single-aisle airplanes.

The production wars continue.

Summary

- Airbus is forecast to out-produce Boeing by 2018.

- Boeing’s ramp-up of the 737 line will drive the delivery stream.

- The 737 rate may hit 63/mo by 2020.

- Airbus will likely match.