Leeham News and Analysis

There's more to real news than a news release.

A321neo configurations and A320 production

By Bjorn Fehrm

18 Jan 2015: As part of the preparations for the Airbus A321LR article 15 Jan. we saw a need to clarify with Airbus the production configurations for A321neo. There had been several iterations of what will be produced come mid-2018 when the A321neo variant is scheduled to roll off the FALs at Airbus in an enhanced Airbus Cabin-Flex (ACF) variant.

This variant features a three-door pairs layout that allows a raised max passenger limit by virtue of displaced door three and an addition of a second overwing exit. Recent media articles have suggested that both the initial four-door variant as well as the three-door variant would be available.

Airbus formally launches A321LR; we look behind the “LR” to see what’s there

15 Jan 2015: Airbus officially launched what to date has been called A321neoLR as the A321LR at their annual press conference Tuesday. The former A321neoLR name was formed by Leeham News on 21 Ocober 2014 when we could reveal the existence of a A321neo variant which Airbus had![]() started to present to airlines at the time. The final name kept the LR attribute used in the article to distinguish the longer range variant from the standard A321neo.

started to present to airlines at the time. The final name kept the LR attribute used in the article to distinguish the longer range variant from the standard A321neo.

The A319 has used the LR designation but its use has been limited. The suffix is more commonly identified with Boeing, used as it is with the 777-200LR. Boeing has also commonly used the ER for extended range like 777-200ER, 737-900ER and 777-300ER.

Interview with John Leahy: A380 sales strategy going forward

Subscription required

Now open to all readers (Fe. 15, 2015)

By Bjorn Fehrm

Introduction

Jan 14 2015: In our deep analysis of the Airbus A380, we concluded that there is nothing wrong with the basic economics of the giant airplane. In fact, with today’s fuel prices, the aircraft’s Direct Operating Costs (DOC) are 20% below![]() its alternatives in the market. Yet the aircraft is experiencing its worst sales drought since its launch, despite adding a leasing alternative during 2014 and efforts by Airbus.

its alternatives in the market. Yet the aircraft is experiencing its worst sales drought since its launch, despite adding a leasing alternative during 2014 and efforts by Airbus.

To understand why and what Airbus plans to do about it we arranged for an exclusive interview with Airbus Chief Operating Officer-Customers, John Leahy, at the sidelines of Airbus annual press conference.

Summary

- Our assessment of A380’s cost of operation

- Operating airlines experience with the A380

- Airbus sales strategy to date and changes going forward

Market potential for A321LR

Here’s how Airbus sees the market potential for the A321LR, going well beyond the 50-60 Boeing 757s flying the Atlantic and some limited operations on other routes.

Airbus believes the A321LR will expand the market considerably over the Boeing 757 long-range routes today. Source: Airbus.

Customer Quality counts as much as orders, says Boeing

Subscription Required

Introduction

Jan. 14, 2015: Customer quality counts as much as the raw number of orders, a top Boeing official said yesterday during a bit of counter-programming on the day Airbus held its annual press conference recapping the previous year’s orders and deliveries.

In a tele-press conference, John Wojick, Boeing SVP of Global Sales & Marketing, said, “It’s not just orders, it’s also about the quality. We work very hard to do business that will actually get to deliveries. We have a much stronger history of orders-to-deliveries than our competitor.”

Summary

- Wojick has a point: Boeing’s customer quality orders historically have been better than Airbus; but

- This is changing. Our Storm Warning Flag assessment shows an improved Airbus customer quality base among the top orders.

- Both companies overbook in anticipation of cancellations and deferrals; Airbus is more aggressive in this practice.

- Airbus had three times the cancellations in 2014 as Boeing.

Odds and Ends: More from Airbus annual press conference; IAM focuses on wages

Jan. 13, 2015: More from Airbus: Airbus held its annual press conference today in Toulouse, reporting its full year 2014 orders and deliveries results. Our Bjorn Fehrm was there and filed a report from the event. He will have more this week. Here are some stories from other media.

Reuters: Airbus to juggle production, defense A380. Airbus says it will likely take A320 production about 50/mo. We reported months ago the supply chain has been notified to prepare for rate 54 in 2018. Airbus also said it will bring A330ceo production down after 2015. We predict 5-6. Decisions are to be made in the coming months.

Bloomberg: Airbus to add 20 passengers to A350-1000.

Aviation Week: Airbus formally launches the A321neoLR. You read this plan here first last October.

Seattle Times: Boeing is No. 1 by some metrics. Dominic Gates takes his usual thorough look at the bragging rights of Airbus and Boeing.

IAM on wages: Boeing’s touch-labor union, the IAM 751, says a Washington State study about aerospace jobs shows 58% of non-Boeing aerospace jobs in the state are paying less than $15 per hour.

Boeing sees little impact from fuel on orders

Jan. 13, 2015: Boeing sees little impact on orders from the falling fuel prices.

In a tele-press conference this morning, Randy Tinseth, vice president of marketing, said recent history shows that even as fuel prices went down, the backlog of orders went up.

Oil is currently hovering around $46/bbl. The last time it was this low was 2008, after the global financial collapse. It took 2 1/2 years for oil prices to recover to around $100/bbl.

Airbus reveals record orders at annual press conference

By Bjorn Fehrm

Toulouse 13 Jan 2015: Airbus today held their annual press conference where they among other things revealed their final numbers for orders and deliveries. The press conference was hosted by Airbus CEO Fabrice Bregier accompanied by COO Customers John Leahy, new COO Tom Williams and new Head of Programs Didier Evrard.

Airbus in 2014

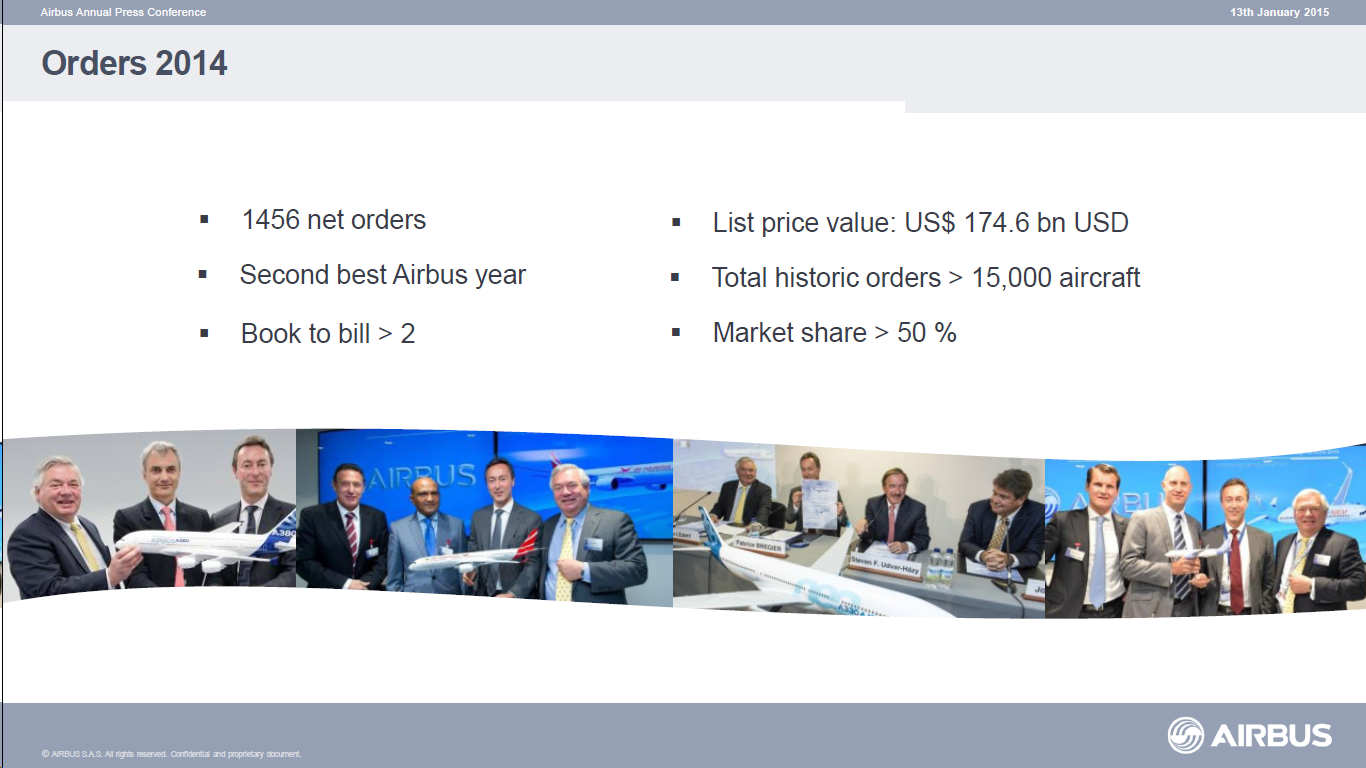

Bregier started with pointing out that 2014 was a very eventful year for Airbus. Airbus did their customary end of year sprint and passed Boeing for net orders with 24 aircraft netting 1456 commands, Figure 1.

Figure 1. Airbus orders for 2014. Source: Airbus.

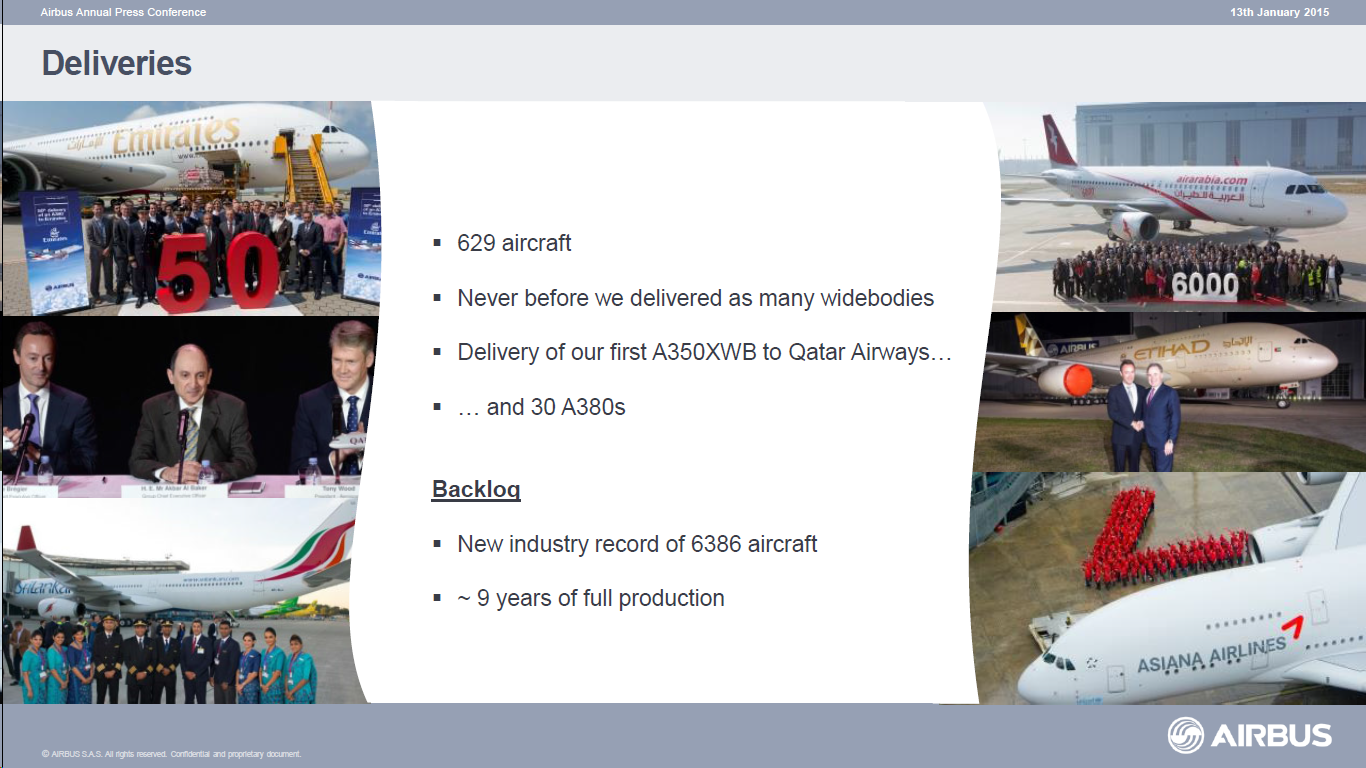

On the delivery side Boeing is ahead with 723 deliveries versus Airbus 629, Figure 2.

Figure 2. Airbus deliveries for 2014. Source: Airbus.

Further Airbus certified the A350 and delivered the first aircraft to its launch customer, Qatar Airways. It also launched the A330neo and got 120 orders during the year. Finally they flew the A320neo first prototype.

A380neo decision likely this year, triggering the next widebody engine project

Subscription required

By Bjorn Fehrm

Introduction

Jan. 12, 2015: One of the subjects which is sure to come up on Airbus annual press conference on Tuesday the 13th in Toulouse will be when and how Airbus will re-engine the A380.

Airbus Commercial CEO Fabrice Bregier vowed during the Airbus Group Global Investors Day last month that an A380neo is coming.

There is much speculation around this subject as the business case of re-engineering an aircraft that is selling at such low numbers is difficult to get to close. The business case is difficult to make work for Airbus ![]() (such a project will cost in the order of $2 billion) but it will be equally hard for the engine manufacturers to offer engines that have enough efficiency gain to make the overall project feasible from an efficiency improvement perspective.

(such a project will cost in the order of $2 billion) but it will be equally hard for the engine manufacturers to offer engines that have enough efficiency gain to make the overall project feasible from an efficiency improvement perspective.

Summary

- A380 Classic equals Boeing 777-300ER seat fuel costs.

- Boeing 777-9 beats A380 on CASM, an A380neo regains the advantage.

- Engine makers face hard choices to retain dominance or to broaden market penetration.